Let’s kick-off the year with a handful of predictions and trends we expect to see in the mobility space in 2020.

Mobility apps move toward aggregation, pursuing super app strategy & profitability

In 2019, the public markets pressured mobility companies to seek profitability. Meanwhile, China’s Meituan — a super app that aggregates multiple micro services for its users — grew sales 44% and turned a profit. In 2020, we’ll see more apps in North America make moves to become the go-to super app. Uber’s CEO has declared intentions to become the Amazon of Transportation, but Uber won’t be the only one.

Continued implosion of carshare companies

Ford shut down Chariot. GM pulled back on Maven. Daimler & BMW announced a billion dollar joint venture. They then shut down ReachNow and Car2Go. Fair laid off 40% of its staff. Getaround has not yet raised their rumored $200M in fundraise. The challenges — and perhaps overhyped valuations — of carshare will continue to play itself out in 2020.

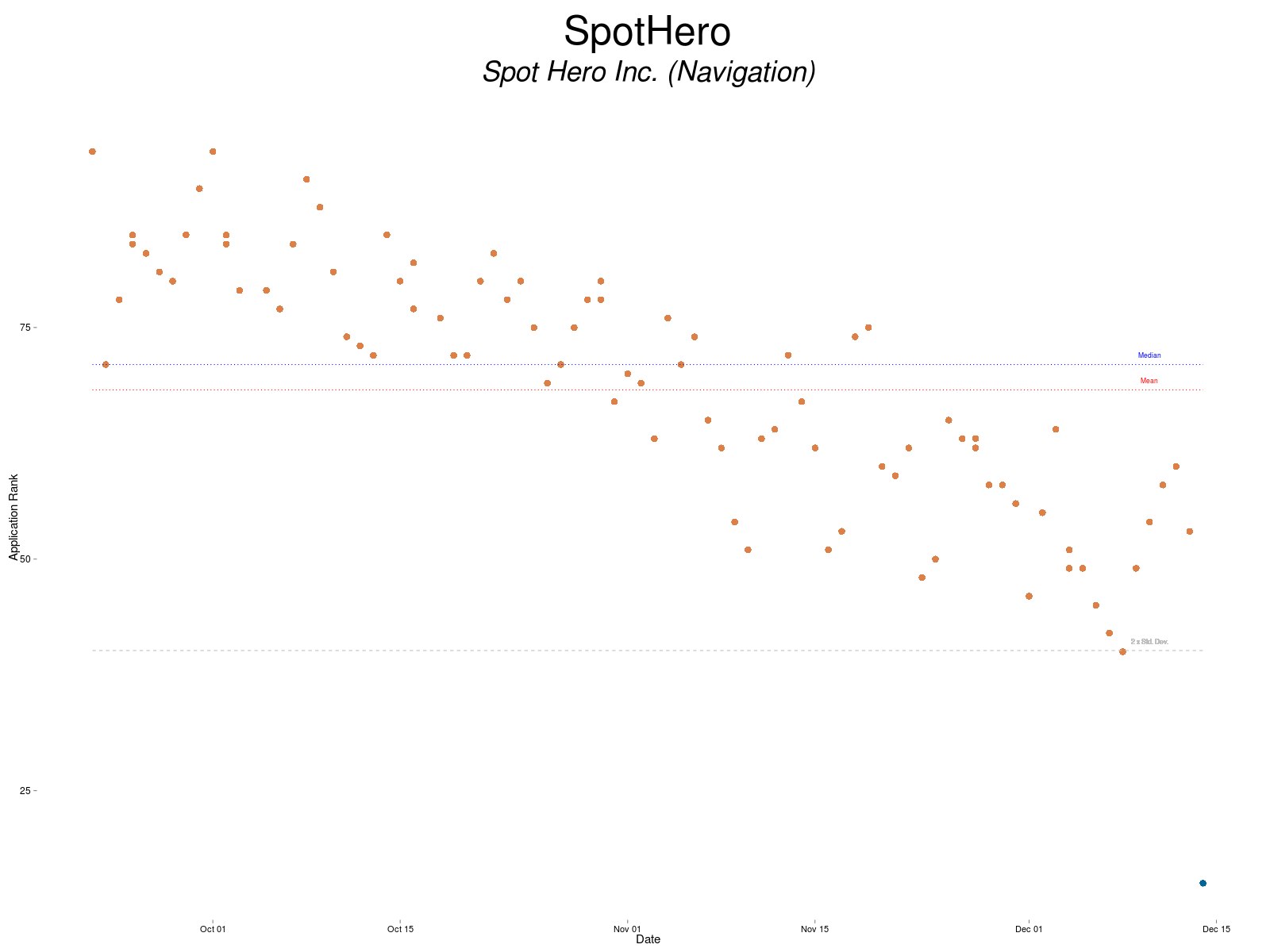

Softbank’s investments in US mobility companies continue to face headwinds

The story is yet to unfold on Softbank’s mobility investments in companies like Getaround, DoorDash, REEF, Mapbox, Nuro and Zume. If 2019 proved anything, it was that capital as a moat failed and the company with the most cash won’t necessarily win.

Startups without market leadership position will begin to consolidate or get acquired

For any mobility company who raised money 18-24 months ago and hasn’t yet raised again, hit profitability or achieved a market leadership position, 2020 may be a challenging year. We may begin to see see more 2nd or 3rd place startups explore acquisitions or announce major cutbacks.

BigTech acquires some winners to fortify moats or expand transportation portfolio

Who knows if WalMart buys FedEx to compete with Amazon, Amazon buys DoorDash after failing to build its own or Apple buys Tesla to expand its mobility footprint, but given the size of the transportation market I’d expect to see a handful of BigTech companies announcing acquisitions of leading growth stage mobility companies.

Resurgence of traditional transportation companies

In 2020, Amtrak could turn a profit for the first time ever. SP Plus, the biggest publicly traded parking management company, saw its stock rise nearly 50% in 2019. Hertz & Avis Budget both saw their stock prices rise as as well following a tough 2018 as well. Perhaps layering good tech on an existing transportation networks may be enough.

OEMs will build great cars, but tech companies will build the connected car platforms

For years OEMs have been seeking to build proprietary connected car solutions. With maybe a handful of exceptions, is anyone really using a connected car app to order pizza yet? At the end of the day, car buyers want access to their iPhone or Android apps in their car — and maybe their favorite voice assistant too.

Prices climb, convenience will trump cost savings

As Barron’s reported this weekend, startups will have to raise fees or prices as investors demand profitability. According to the report, “Lyft and Uber fares were up 6% on average since May.” At the same time, experimentation shows higher fees slows ridership so there’s a delicate balance.

Commerce apps expand to new verticals, information apps add commerce

In 2020 and beyond, we’ll see a) commerce-based apps continue to expand horizontally to add more verticals (apparently including skiing) and b) information-based apps seek more ways to monetize their audience with commerce.

Partnerships that solve end-to-end multi-modal solutions will win

Product partnerships that delight users by simplifying or enriching the transportation experience will win. Partnerships that are nothing more than a press release, a logo on a slide and some advertising space in two disjointed experience will continue to fail. Why would you go into a third party app for paired down mobility experience when you can just go directly to the app for the full experience? Look for partnerships that create a more delightful user experience, add commerce at relevant touch points and/or reduce the friction of jumping between multiple apps for one journey.

Of course, there’s so much more …

Will we actually have self-driving cars any time soon? Could climate concerns accelerate EVs, or other solutions that get cars off the road faster? Has Tesla finally turned a corner? Will cities continue to eliminate on-street parking? Will on-demand buses actually work? What will happen with gig economy regulation?